Inefficiency

Inefficiency

Under certain circumstances, firms in market economies may fail to produce efficiently. Inefficiency means that scarce resources are not being put to their best use. In economics, the concept of inefficiency can be applied in a number of different situations.

Pareto inefficiency

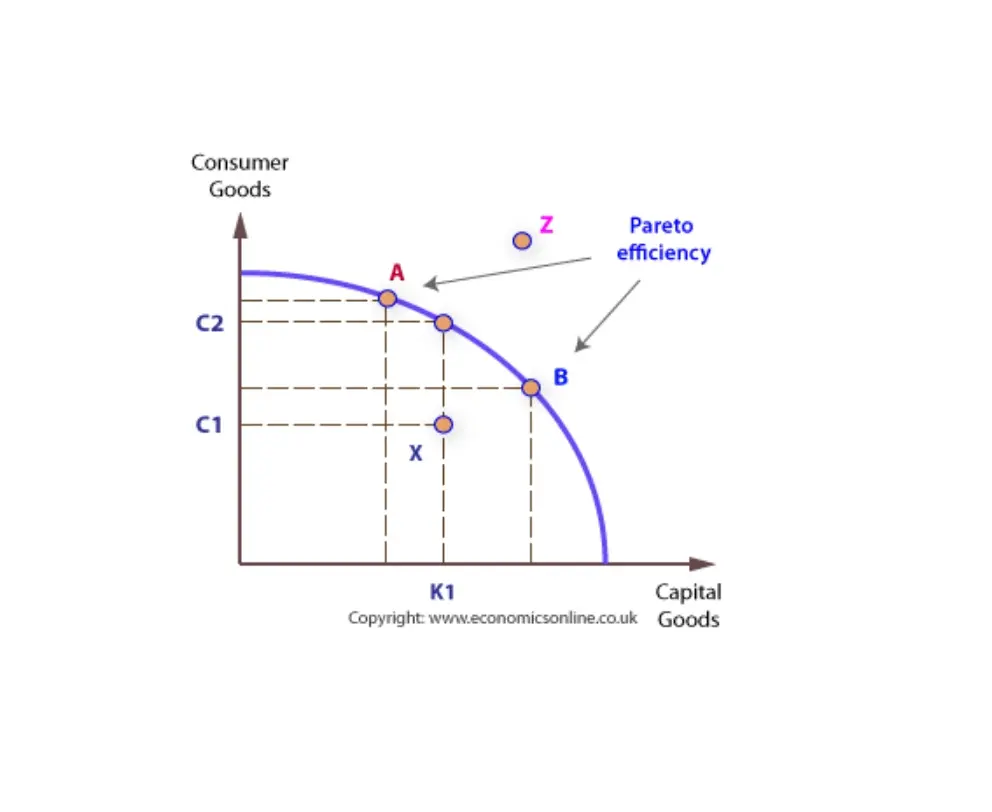

Pareto inefficiency is associated with economist Vilfredo Pareto, and occurs when an economy is not operating on the edge of its PPF and is, therefore, not fully exploiting its scarce resources.

This means that the economy is producing less than the maximum possible output of goods and services, from its resources.

Productive inefficiency

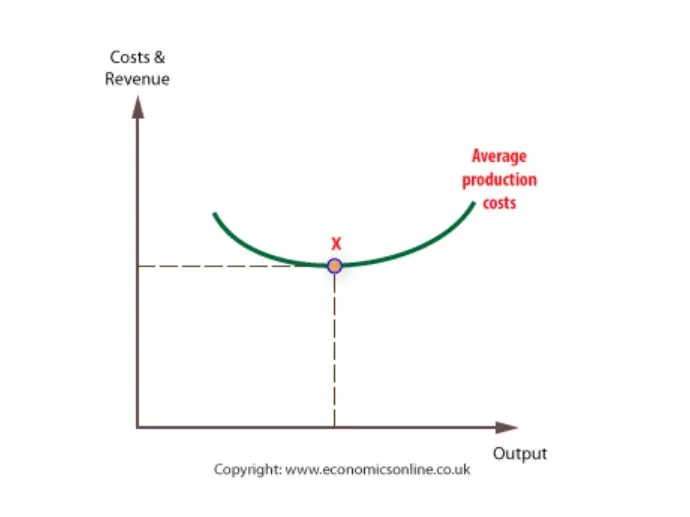

Productive inefficiency occurs when a firm is not producing at its lowest unit cost. Unit cost is the average cost of production, which is found by dividing total costs of production by the number of units produced.

It is possible that in markets where there is little competition, the output of firms will be low, and average costs will be relatively high. This is likely to occur if a few firms, or just one, dominate the market, as in the case of oligopoly and monopoly.

‘X’ inefficiency

‘X’ inefficiency is a concept that was originally associated specifically with management inefficiencies, but can also be applied more widely.

X inefficiency occurs when the output of firms is not the greatest it could be. It is likely to arise when firms operate in highly uncompetitive markets where there is no incentive for managers to maximise output.

Allocative inefficiency

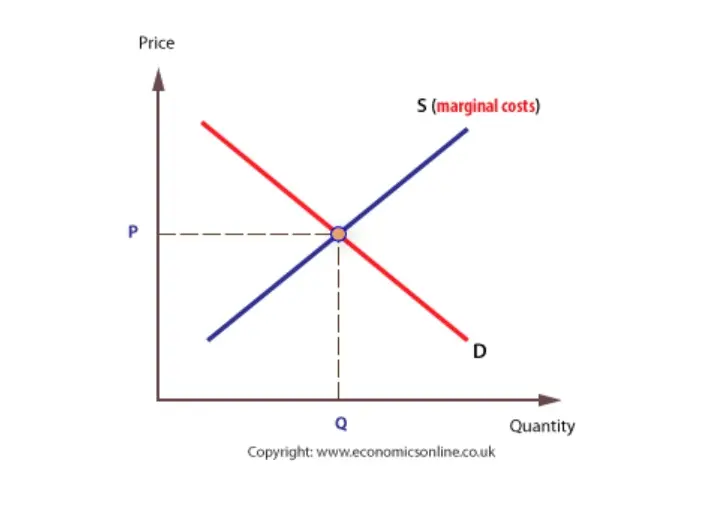

Allocative inefficiency occurs when the consumer does not pay an efficient price.

An efficient price is one that just covers the costs of production incurred in supplying the good or service.

Allocative efficiency occurs when the firm’s price, P, equals the extra (marginal) cost of supply, MC. This is efficient because the revenue received is just enough to ensure that all the resources used in the making of a product are sufficiently rewarded to encourage them to continue supplying.

Receiving the value of marginal cost – no more and no less – is economically efficient because all factors derive a reward which just keeps them supplying their resource, including a normal profit for the entrepreneur.

Dynamic inefficiency

Dynamic inefficiency occurs when firms have no incentive to become technologically progressive. This is associated with a lack of innovation, which leads to higher production costs, inferior products, and less choice for consumers.

There are two ways in which firms can innovate:

- New production methods, such as when applying new technology to an existing process.

- New products, which are a feature of markets with highly competitive firms, such as those in the consumer electronics.

Innovation, research, and development are expensive and risky, so firms will expect a fair level of profits in return. However, because the price mechanism may not generate profits for the supply of public and merit goods, there is often an absence of dynamic efficiency in these markets.

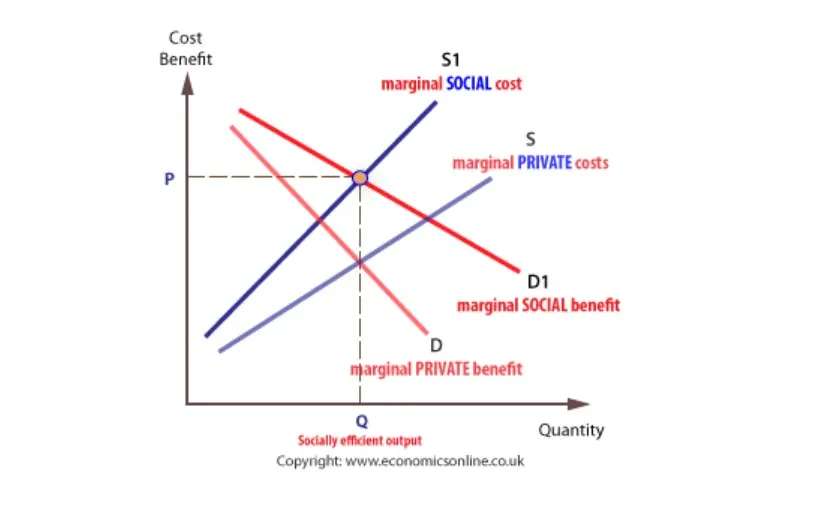

Social inefficiency

Social inefficiency occurs when the price mechanism does not take into account all the costs and benefits associated with economic exchange.

The price mechanism will only take into account private costs and benefits arising directly from production and consumption, not the external costs and benefits incurred by third–parties.

Social costs refer to the total costs borne by society as a result of an economic transaction, and include private costs plus external costs. Social benefits are the private benefits plus external benefits resulting from a transaction.

A transaction is socially efficient if it takes into account costs and benefits associated with the transaction – that is, the social costs and benefits.

Go to: Cost-Benefit Analysis (CBA)