Nvidia Faces Valuation Test as AI Capex Nears Peak

Even with Nvidia's record revenue achieved in the latest quarter, surpassing market estimates and a very positive outlook for the current quarter, its stock price has dropped since then. The stock has lost 7% in value over the last week and 4.2% since the beginning of the year. Investors are questioning whether AI infrastructure capital expenditures are close to peaking. The slowing of this cycle will lead to revenue growth rates starting at 65% in FY23 and declining over time to 30% in FY24 and from 13% to 14% thereafter. Any company whose valuation is based on extant exponential growth visions will see valuation metrics starting to decline as a result of these dynamics.

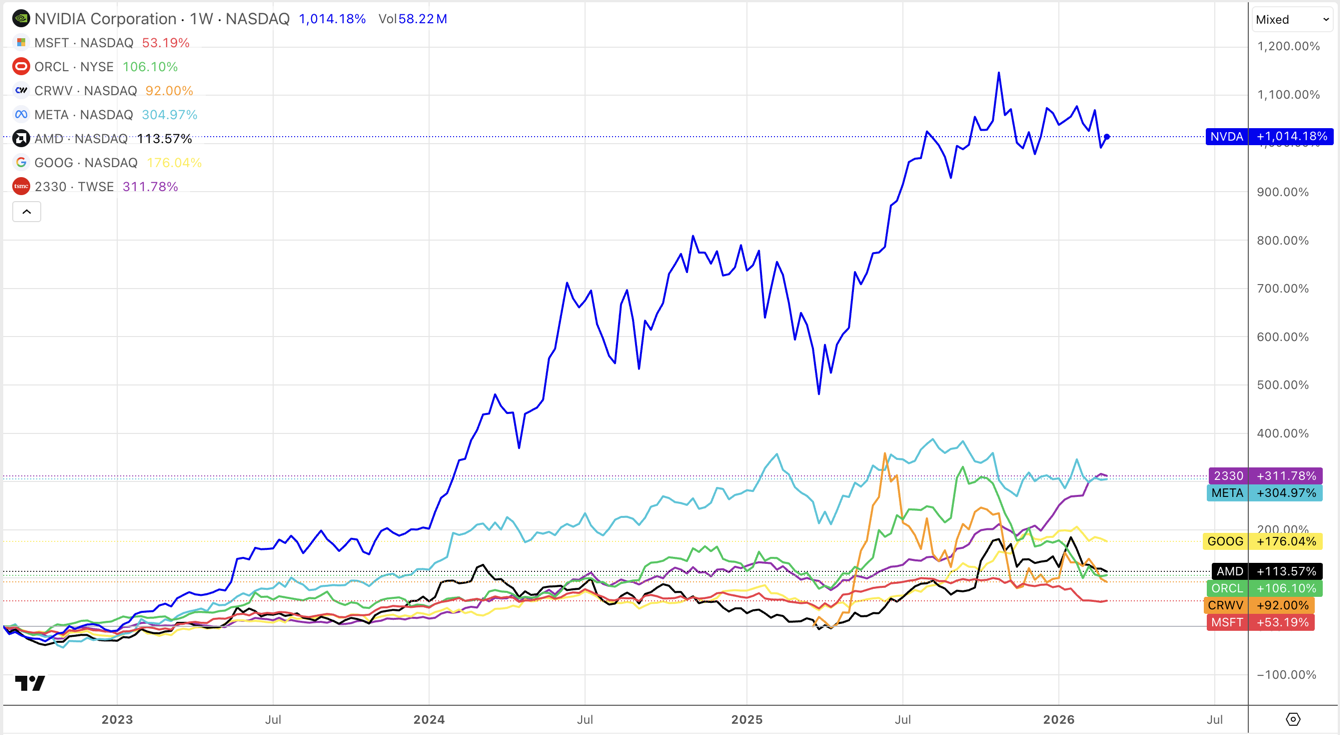

At this point, customer diversification is increasing. OpenAI rents Trainium-based capabilities from Amazon Web Services (AWS) and continues to source compute from Microsoft, Oracle, and CoreWeave, in addition to partnering with Cerebras. Nvidia remains the dominant player in this category; however, emerging alternatives will shift bargaining power and place limits on the long-term margins that have historically been very high. For example, large customers such as Meta Platforms are also testing AMD and Google components to diversify their reliance on a single vendor.

Following Nvidia’s earnings report, investor sentiment toward the tech industry appears to be shifting. After the report was released, Dow Jones futures and other major U.S. indices showed little movement, suggesting increasing caution among investors in the tech sector. Investors focused on potential future risks such as peak infrastructure costs and slowing growth rates rather than the strong revenue numbers reported in the quarter. As a result, Nvidia’s stock appears to be driven more by expectations about how the AI cycle will influence long-term corporate investment than by the company’s most recent performance.

The financial stability of these partner companies has become increasingly intertwined. By the end of this year, Nvidia has become TSMC’s largest customer, representing 22% of total revenue ($23.2 billion), compared with Apple’s 17% share. This change in TSMC’s customer leadership reflects a broader shift in global technology value away from consumer electronics and toward artificial intelligence (AI) infrastructure.

However, this dominance hides an increasing risk. Nvidia's procurement The company's contractual obligations have risen significantly, from roughly $16 billion per year to $95 billion as of year-end, with an estimated value of $117 billion—approximately equal to cash flow from operations. As noted by investor Michael Burry, this structure resembles that of the dot-com era, when excessive optimism about demand led to rising financial liabilities.

Assuming demand for accelerators declines, Nvidia will still be obligated to pay for both capacity and components even if utilization falls short, potentially placing pressure on both cash flow and margins.

A paradox begins to emerge: the greater the demand today and the higher the price of accelerators, the greater the future obligations created for the company, increasing operational leverage. Conversely, as the AI market continues to grow, this model can generate peak profitability. However, when the economic cycle turns, these financial commitments may amplify the downside. This helps explain why investors are becoming increasingly cautious, as they begin to discount not only current results but also the risk of a future economic slowdown.

The potential for price corrections driven by cyclical trends could create greater volatility and losses in these markets and may also delay the IPOs of OpenAI and Anthropic IPO. Both companies can be considered highly speculative investments, particularly given Nvidia’s investment stake in them.

Having benefited from some of the largest capital inflows ever seen in the technology industry, these firms also represent significant risk. Their business models rely heavily on high-volume production through a single manufacturer, substantial prepayment commitments, and the evolving possibility that alternative computing architectures may emerge.

As a result, investors may need to shift from euphoric sentiment toward a more fundamental evaluation focused on cash flows, long-term liabilities, and margin stability, particularly if the AI market experiences a correction following the next wave of IPOs.