An image showing a barrier.

Barriers to Entry

Definition

The hurdles, obstacles, and challenges faced by new firms when they try to enter a specific market or industry are called barriers to entry. These are the factors that make it difficult for new firms to enter an industry.

For example, in the automotive industry, high capital requirements, extensive distribution networks, and established brand loyalty make it difficult for new firms to enter the industry and compete with established car manufacturers.

Types of Barriers to Entry

There are many types of barriers to entry. Some major types are explained below.

Primary Economic Barriers

Primary economic barriers to entry are factors that make it difficult for new firms to enter a market based on economic considerations. These barriers include high start-up costs, economies of scale enjoyed by existing firms, and limited access to distribution channels.

For example, in the airline industry, high costs associated with purchasing aircraft, establishing routes, and building infrastructure create significant barriers for new airlines. Additionally, existing airlines benefit from economies of scale, such as purchasing fuel in bulk, which gives them a cost advantage over new firms. Limited access to airport slots and gates also makes it challenging for new airlines to secure desirable locations and compete effectively.

Types of Primary Economic Barriers

Primary economic barriers to entry can be classified into three main categories:

Cost-related Barriers

These barriers arise from the high costs involved in entering a market. Examples include the need for significant capital investment, expensive research and development, or expensive marketing and advertising campaigns. These costs can deter potential new entrants from competing with established companies.

Scale-related Barriers

Scale-related barriers occur when existing firms benefit from economies of scale, which are cost advantages that come with producing on a large scale. Established companies can spread their fixed costs over a larger output, leading to lower average costs. This can make it difficult for new firms to compete on price or match the efficiency of established players.

Access-related Barriers

Access-related barriers arise when new entrants face difficulties accessing essential resources or distribution channels. This includes limited access to key suppliers, exclusive contracts with distributors, or regulatory barriers that restrict market entry. These barriers can limit the ability of new companies to compete effectively.

Structural Barriers

Structural barriers refer to obstacles that arise from the structure or characteristics of a market or industry.

There are several types of structural barriers.

Regulatory Barriers

These barriers result from government regulations and policies that restrict or control market entry. Examples include licencing requirements, permits, certifications, and compliance with specific industry standards.

Intellectual Property

Intellectual property rights, such as patents, copyrights, and trademarks, can create barriers to entry by granting exclusive rights to certain inventions, creative works, or brand names. This prevents others from entering the market with similar products or services.

Network Effects

Network effects occur when the value of a product or service increases as more people use it. This creates a barrier to entry because new businesses may struggle to attract users if an existing network is already well-established. Examples include social media platforms and online marketplaces.

Brand Loyalty

Established brands with strong customer loyalty can create barriers to entry. Consumers may be hesitant to switch to new, unknown brands, especially if they have a strong attachment to or trust in the existing brand.

Economies of Scale

Economies of scale occur when the average cost of producing a product decreases as output increases. Existing firms that have already achieved high production levels can benefit from lower costs, making it difficult for new firms to compete on price.

Distribution Channels

Limited access to distribution channels can act as a barrier to entry. Established companies may have exclusive agreements or long-standing relationships with distributors, making it challenging for new firms to secure distribution for their products.

Natural Barriers to Entry

Natural barriers to entry are obstacles that arise from the inherent characteristics of a market or industry. These barriers are not created by the intentional actions of existing firms but are instead the result of natural circumstances.

Unlike structural barriers, which can be influenced by existing firms in the industry, natural barriers are typically beyond the control of existing market participants. Natural barriers arise from various factors related to the industry itself, and they can significantly impact a new entrant's ability to establish a foothold. There are several types of natural barriers to entry:

Access to Essential Resources

When an industry relies on rare or limited raw materials, new firms may struggle to secure a stable supply, especially if existing firms have long-term contracts or established relationships with suppliers.

Technological Barriers

In technology-driven industries, established firms often possess advanced technological capabilities and intellectual property rights that are difficult for new firms to replicate. Moreover, developing new technologies and products can require significant investments in research and development, which can be a natural barrier for smaller or new companies.

Regulatory Barriers

Some industries are subject to stringent government regulations, licencing requirements, or safety standards. Compliance with these regulations can be time-consuming and costly for new entrants.

Moreover, industries reliant on patents, copyrights, or trademarks may have natural barriers in the form of intellectual property protection, which can limit the ability of new competitors to use or replicate proprietary technologies or brand identities.

Network Effects

In industries where the value of a product or service increases as more people use it (e.g., social media platforms), established companies with a large user base have a natural advantage over new firms trying to build their networks from scratch.

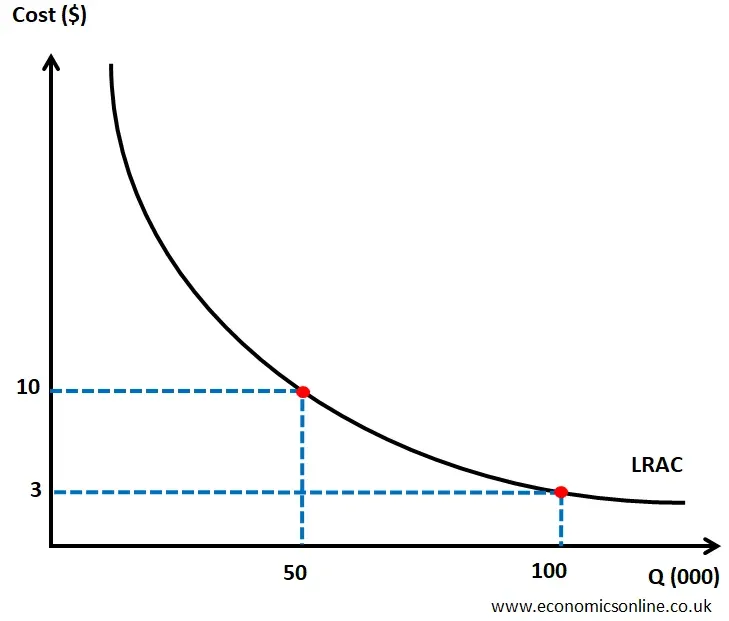

Natural Monopoly

A monopoly which is made because of cost structure is called natural monopoly. It is made when long run average cost (LRAC) can be decreased and economies of scale are possible only when output of the whole industry is produced by one firm. It means that the most efficient number of firms in an industry is one in the entire market. Hence, new firms cannot enter the industry. The following example and graph can explain natural monopoly.

Suppose that the market demand is of 100,000 units for a particular product. If one firm produces 100,000 units, its LRAC will be $3. If two firms produce 50,000 units each, the average cost will be $10. The only way to have low LRAC is that the output of whole industry should be produced by one firm. Hence, the optimal number of firms is 1. This firm will be natural monopoly and it will naturally act as an entry barrier.

Strategic Barriers

Strategic barriers are the obstacles intentionally created by firms to protect their market position and deter potential competitors. These barriers are the part of firm’s strategic planning and take various forms.

These artificial barriers are often anti-competitive in nature and aim to protect the market power and profitability of incumbent firms. Some examples of these barriers to entry include.

Exclusive Contracts

Existing firms may establish exclusive contracts with suppliers, distributors, or retailers, preventing new firms from accessing these essential resources or channels.

Intellectual Property Abuse

Existing firms may misuse or abuse their intellectual property rights, such as filing frivolous lawsuits or engaging in patent trolling, to deter new firms from entering the market.

Predatory Pricing

Established firms may engage in predatory pricing, where they temporarily set prices below cost to drive out competition and discourage new businesses from entering the market.

Regulatory Capture

Existing firms may exert influence over regulatory bodies or government agencies to create regulations or policies that favor their interests and create barriers to entry for potential competitors.

Brand and Reputation

Established brands and strong reputations can act as barriers to entry for new entrants. Consumers may have loyalty or trust in existing brands, making it difficult for new entrants to gain market share.

Industry-Specific Barriers

Industry-specific barriers refer to obstacles that are unique to a particular industry and can make it difficult for new entrants to compete.

These barriers can vary depending on the characteristics and dynamics of the industry.

Regulatory Requirements

Certain industries, such as healthcare, finance, or telecommunications, have strict regulatory requirements that new entrants must comply with. These regulations can include licensing, permits, certifications, and compliance with specific standards. Meeting these requirements can be time-consuming and costly, acting as a barrier to entry.

High Capital Requirements

Some industries, like manufacturing or infrastructure development, require significant upfront investment in equipment, machinery, facilities, or technology. The high capital requirements can deter new entrants who may not have the financial resources to make such investments.

Intellectual Property Rights

Industries that heavily rely on innovation and intellectual property, such as pharmaceuticals or technology, often have strong patent protection for inventors. This can make it challenging for new entrants to develop similar products or technologies without infringing on existing the legal rights of patents.

Distribution Networks

Industries with well-established distribution networks, such as retail or consumer goods, can pose challenges for new entrants. Established companies may have extensive networks of suppliers, distributors, and retailers, making it difficult for newcomers to access these channels and compete effectively.

Brand Loyalty

Industries where brand loyalty plays a significant role, such as fashion, beauty, or food and beverages, can present barriers for new entrants. Established brands often have a loyal customer base and strong brand recognition, making it challenging for new competitors to gain market share.

Expertise and Knowledge

Some industries require specialised knowledge, expertise, or technical skills. Examples include aerospace, biotechnology, or engineering. New entrants may face difficulties in acquiring the necessary expertise or building a team with the required skills, acting as a barrier to entry.

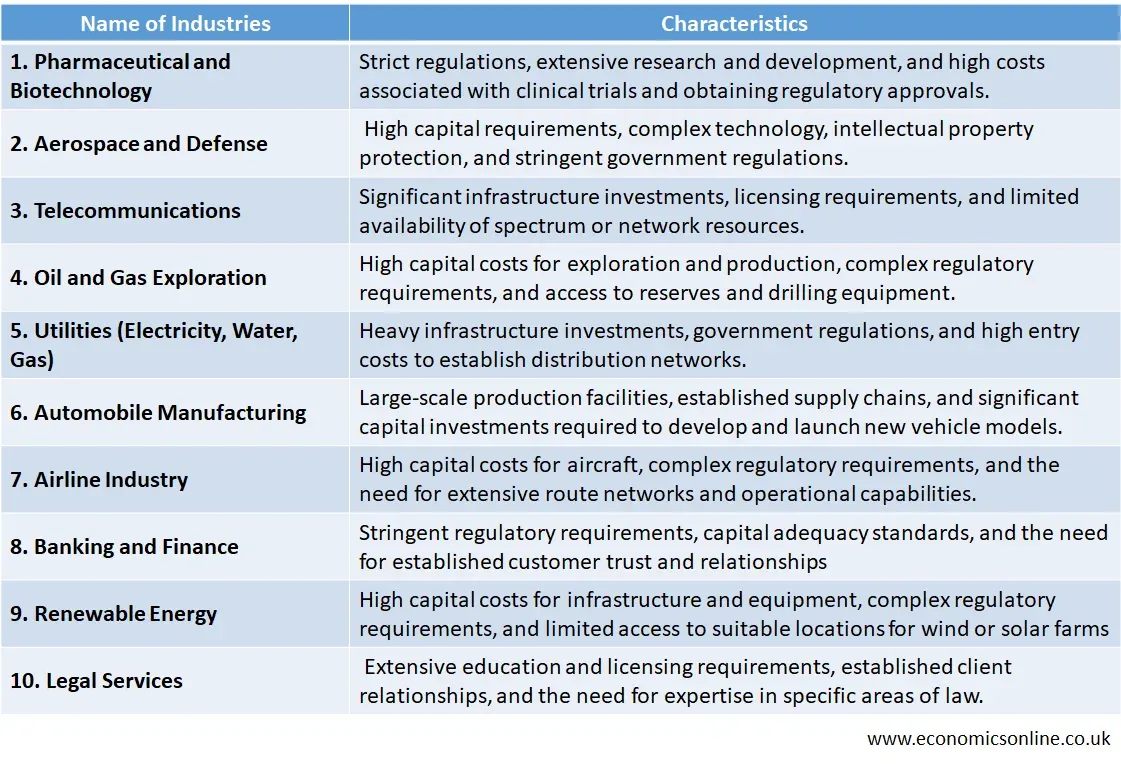

Industries Having High Barriers to Entry

The following table summarises the entry barriers in some important industries including pharmaceuticals, defense, telecommunication, utilities and many more.

Government Barriers to Entry

Government barriers to entry are the hurdles which governments create to make it difficult for new firms to enter an industry. There barriers are imposed by governments to protect existing firms from new competitors, specially the domestic firms from foreign competitors, to ensure safety and quality standards and to avoid duplication of resources through wasteful competition. Many other reasons are also possible.

These barriers can include.

Licensing and Permits

Some industries require specific licenses or permits to operate, which can be time-consuming and costly to obtain.

Regulatory Requirements

Compliance with government regulations, such as safety standards or environmental regulations, can pose challenges for new entrants.

High Taxes and Fees

Governments may impose high taxes or fees on certain industries, making it difficult for new businesses to compete.

Intellectual Property Protection

Intellectual property laws and patent regulations can create barriers for new entrants trying to bring innovative products or technologies to market.

Subsidies and Grants

Existing companies may benefit from government subsidies or grants, giving them a competitive advantage over new entrants.

Trade Barriers

Governments may impose trade restrictions or tariffs that limit competition from foreign companies.

Access to Government Contracts

Established companies may have an advantage in securing government contracts, limiting opportunities for new entrants.

Lobbying and Political Influence

Existing industry players may have strong political connections, making it challenging for new entrants to compete on a level playing field.

How to Overcome Barriers to Entry?

To overcome barriers to entry in an industry, firms can consider the following strategies.

Differentiation

Develop a unique product or service that sets you apart from existing competitors and attracts customers.

Cost leadership

Find ways to lower production costs or offer competitive pricing to gain a cost advantage over established players.

Technology and Innovation

Utilise advanced technology, research and development (R&D) to create new products, improve efficiency, or disrupt traditional industry practices.

Strategic Partnerships

Collaborate with existing companies or form alliances to leverage their resources, expertise, and customer base.

Market Niche

Identify under-served or niche markets that are not adequately addressed by existing players and tailor your offerings to meet their specific needs.

Brand Building

Invest in building a strong brand reputation and customer loyalty to compete against established brands.

Access to Capital

Secure sufficient funding or investment to overcome initial financial barriers and sustain operations during the early stages.

Intellectual Property Protection

Obtain patents, trademarks, or copyrights to protect your unique ideas, inventions, or brand identity.

Persistence and Resilience

Be prepared for challenges and setbacks, stay focused on your goals, and continuously adapt your strategies to overcome obstacles.

Difference between High and Low Barriers to Entry

Accessibility

Low barriers to entry mean that new firms can easily enter the market. High barriers make it difficult for new entrants to establish themselves.

Competition

Low barriers to entry encourage competition, leading to a greater number of firms competing for market share. High barriers to entry limit competition, allowing existing firms to maintain their market dominance.

Innovation

Low barriers to entry often foster innovation as new firms bring fresh ideas and approaches to the market. High barriers can stifle innovation, as established firms may have less incentive to innovate without competition.

Market Power

Low barriers to entry prevent any single firm from having excessive market power, promoting a more balanced and competitive market. High barriers can result in the concentration of market power in the hands of a few dominant firms.

Consumer Impact

Low barriers to entry generally benefit consumers by offering more choices, lower prices, and improved product quality. High barriers can limit consumer options, potentially leading to higher prices and reduced product variety.

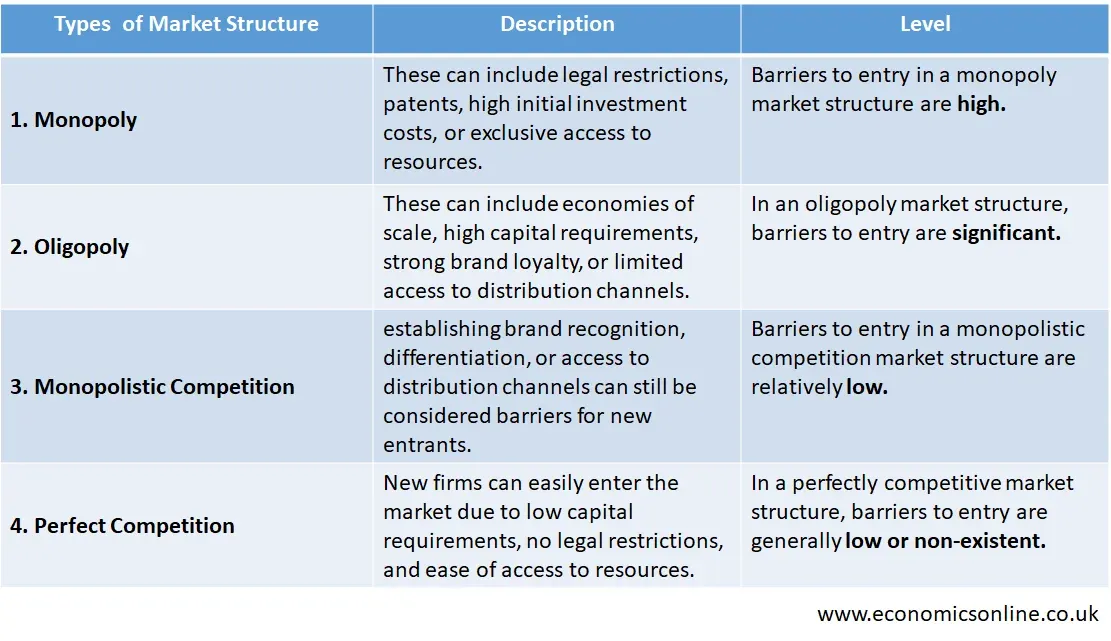

Barriers to Entry in Different Market Structures

The following table summarises the level and intensity of entry barriers in different types of market structures including monopoly, oligopoly, monopolistic competition and perfect competition.

Barriers to Exit

Here are a few key points about barriers to exit.

Sunk Costs

Sunk cost is a cost which cannot be recovered once it is incurred. Firms may have invested significant resources, such as legal cost, marketing cost or time, into the market, creating sunk costs that are difficult to recover if they exit.

Contractual Obligations

Businesses may have contractual commitments with suppliers, customers, or employees that make it complicated or costly to exit the market prematurely.

Specialised Assets

Some industries require specific assets or infrastructure that may have limited alternative uses. Exiting the market would mean losing the value of these specialised assets.

Reputational Concerns

Firms may be hesitant to exit a market due to concerns about damaging their reputation or the perception of failure.

Regulatory Barriers

Regulatory requirements or government restrictions can also act as barriers to exit, making it challenging for firms to wind down operations or exit the market.

Conclusion

In conclusion, barriers to entry are the difficulties faced by new firms when they try to enter a market. Low barriers to entry promote competition, innovation, and consumer choice, while high barriers to entry can limit competition and allow existing firms to maintain market power. On the other hand, barriers to exit can make it difficult for firms to leave a market, potentially leading to continued operation despite unfavorable conditions. Understanding these barriers is important for analysing market competitiveness, the type of market structure and the potential for new entrants to disrupt existing firms.

![Which Tools Do Economic Analysts Rely On [Financial Analysis Software]](/content/images/size/w600/2024/09/Untitled-design-6.webp)