Monetary theory

Money and monetary theory

Money is any asset that is acceptable in the settlement of a debt. For an asset to be widely used as money, it should be portable, divisible, durable and stable in value.

Some assets fulfill the role of money much better than other ones. Gold and silver have frequently been used as money, given their divisibility into bars and coins. The introduction of paper money by the Chinese marked a significant development in the evolution of money, especially given the ease with which different denominations could be created, and the portability of paper money in comparison with gold or coinage.

The advent of money as a medium of exchange replaced the need for exchange through barter and enabled producers and factor owners to specialise and sell their output for money. The money earned could then be used to trade with other producers and factor owners. It is clear that the evolution of money as a medium of exchange, and as a store of wealth, had a considerable impact on the development of modern economic commerce, international trade, and global prosperity.

In modern economies, notes and coins represent only a small fraction of the total money supply, with most money being in the form of digital bank accounts.

Money supply

Money can be created in a number of ways:

- Money is created whenever banks give new loans to customers, triggered by new cash deposits in their bank. New bank deposits can create a multiple credit expansion throughout the banking system, increasing liquidly and enabling fresh loans to be made as a multiple of the original deposit. In effect, money increases when fresh loans are advanced to customers. The formula to calculate how much extra credit can be given is called the credit multiplier and is 1/Cash Ratio. For example, if the cash ratio is 0.1, the credit multiplier is 1/0.1 = 10, and a fresh cash deposit of £1,000 could lead to fresh advances to customers of £10,000. This is because the new deposit of £1000 need only represent 10% of total monetary assets. This means that each new £1 received by the bank could be used to generate £10 of credit in the form of advances to other customers.

- Secondly, issuing Treasury bills can also add to the money supply, and this happens when the government borrows from the money market by issuing Treasury bills. Banks treat these bills as being ‘as good as cash’, and continue to make the same amount of loans to their customers. This is despite the fact they have lost liquidity by buying bills from the Treasury. The net effect is that money supply in the economy increases.

- Thirdly, the central bank, the Bank of England, can print new money if the normal flow of liquidity is disrupted, as in the recent financial crisis. The Bank can use this new money to buy up existing government debt, including bonds held with private firms, so injecting new liquidity into the system. This process is called quantitative easing.

Measuring the money supply

Money is officially measured in narrow terms or broad terms.

Narrow money and broad money

M0 (M nought) is the official measure of narrow money in the UK and consists of notes and coins in circulation outside the Bank of England, plus bankers’ operational deposits with the Bank. The main reason for identifying M0 is its close link with high street spending, and inflation. M0 is also called ‘high powered’ money because of its strong impact on the economy.

M4

M4 is the favoured measure of broad money and includes:

- Cash (notes and coins) in circulation with the public and firms other than banks;

- Private sector retail bank and building society deposits;

- Private sector wholesale bank and building society deposits;

- Certificates of deposit.

Cash represents only 2.6% of broad money (2016), as the chart indicates.

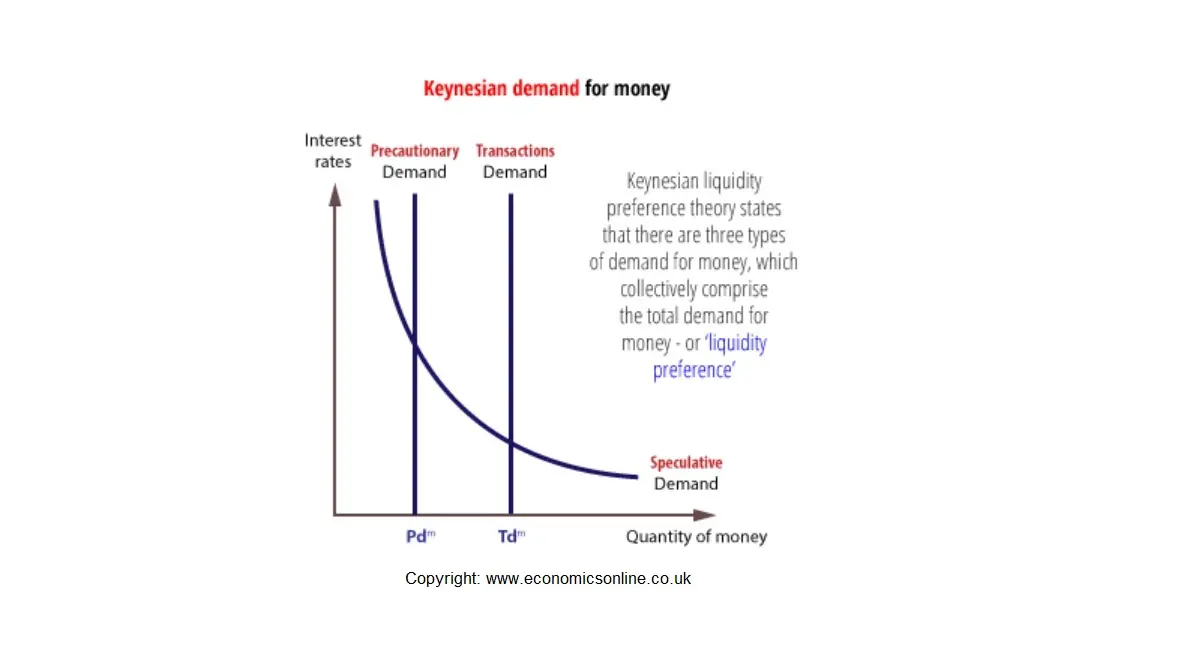

The demand for money

According to Keynes’ Liquidity Preference theory, people demand money, that is liquidity, and hold their wealth in a monetary form for three reasons:

- To engage in real transactions

- As a precaution in the event of unexpected spending

- To engage in speculative transactions

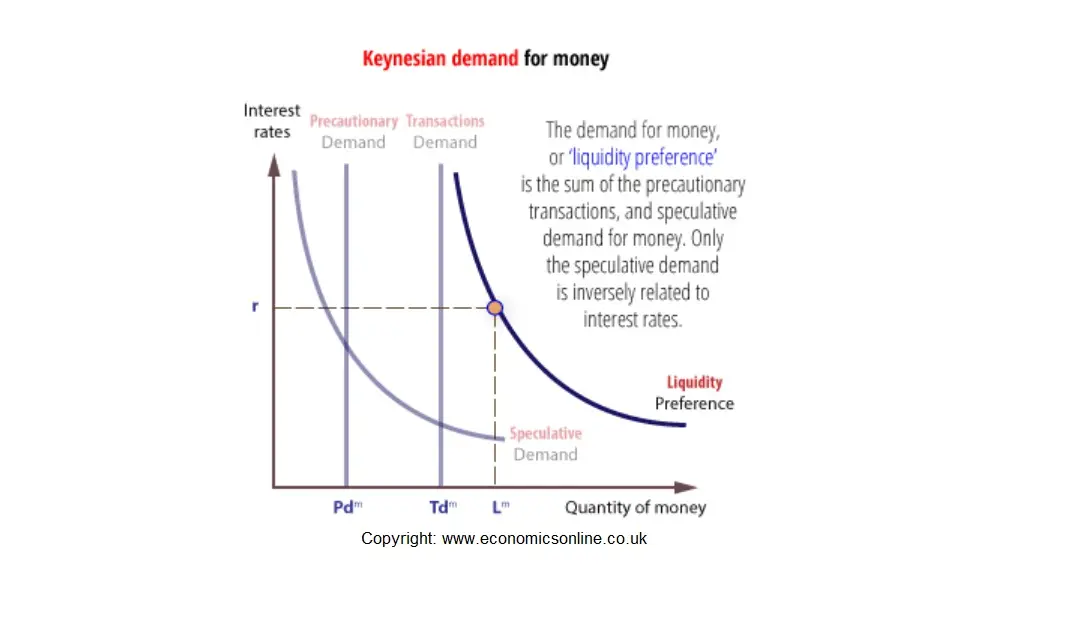

The demand for money

The different components of the demand for money can be plotted against interest rates. Together, they represent the demand for money, which may also be called ‘liquidity preference’.

Both the transactions demand and the precautionary demand are unrelated to interest rates and are shown as vertical curves. However, according to Keynes’ liquidity preference theory, the speculative demand for money – that is, the desire to hold money to gain a speculative return as an alternative to other forms of speculation – is inversely related to interest rates.

Keynes illustrated the concept by considering the demand for money as an alternative to holding government bonds, which have fixed rates of interest. Bond prices and general interest rates are inversely related, so that a rise in the interest rate on new bonds issued will lead to a fall in the price of existing bonds. A speculator will only buy existing bonds at a fixed (lower) rate if the price of existing bonds falls to make it worthwhile and a realistic alternative to buying new bonds at a higher fixed rate. Therefore, if we look at the speculative demand for money, at very low interest rates, speculators tend to predict that the next movement in interest rates is upwards, and, therefore, the next movement in bond prices is downwards. Because of this speculators will prefer to hold their assets in a monetary (liquid) form rather than in bonds, which would result in a speculative loss. Therefore, at low interest rates the speculative demand for money is very high and approaching infinite elasticity. Clearly, government bonds are not the only alternative to money, but the concept is still relevant.

The overall liquidity preference curve for an economy, that is the combined demand for money for transactions, as a precaution, and for speculative purposes, is downward sloping against interest rates.

Money supply

If we add the money supply, we can find the equilibrium interest rate. In simple Keynesian theory, the supply of money is unaffected by interest rates, so the money supply curve (M) is vertical, as shown below. Money market interest rates will be the rate that brings demand and supply into equilibrium. For example, the money market will clear when interest rates are 4% – with the supply of money (M) equalling the demand for money (L).

The supply of money

The different components of the demand for money can be plotted against interest rates.

The money supply is controlled by the Bank of England, and is independent of interest rates.

Modern money markets

The UK money market includes banks, building societies, and specialist securities dealers who buy and sell money. The market is controlled by the Bank of England, and regulation is shared between the Bank of England, the Treasury, and the Financial Services Authority (FSA).

Monetarism

Monetarism is closely associated with Classical economics and is an economic philosophy which believes that economic prosperity depends upon understanding and manipulating the link between money and the real economy – that is, prices, output and employment. In addition, monetarism stresses the effective control of the money supply as the main method of stabilising the macro-economy.

Although monetarism dates back to English philosophers of the 18th Century, its modern origins can be traced to the work of Irving Fisher of Yale University, writing in the early 20th century. Modern quantity theorists, including Milton Friedman of Chicago University, developed Fisher’s work further.

Monetarists, such as Friedman, believe that:

- Money can be defined – money is defined as ‘anything generally acceptable with which to settle a debt’.

- Money can be controlled – monetary authorities can increase or decrease the amount of money in the economy.

- Changes in money have a direct and measurable effect on the rest of the economy – indeed, the money supply has a significant effect on the spending of households and firms.

- Inflation and deflation are always and everywhere a monetary phenomenon – changes in money are always the cause of price changes.

Money and inflation – The Fisher equation

Fisher proposed that there was a stable and predictable relationship between the quantity of money in circulation in an economy, and the price level, using his famous equation:

MV = PT, where:

M = the stock of money

V = the velocity of circulation

P = average prices

T = the number of transactions

If we assume V and T are constant, as the economy approaches full employment, then changes in M must lead to the same proportionate changes in P.

The main policy implication is that the monetary authorities should ensure that money supply is effectively controlled, because controlling the money supply means that average prices can be stabilised.

Controlling the money supply

Despite the difficulties of directly manipulating the economy through interest rates, especially in a recession, authorities usually find that, under normal economic conditions, it is easier and more effective to influence interest rates than control the money supply.

There are several reasons for this, including:

Money is difficult to define and control

Money is not always easy to measure, or at least it is not easy to agree which measure to use. Any asset could be used to settle debts, so new forms of money can be introduced that cannot easily be controlled.

Unpredictable effects

Changes in the money supply, or a component of the money supply, do not always have a predictable effect on the inflation rate. One explanation for this is contained in Goodhart’s Law. This states that, once a particular instrument is used for policy purposes, the relationship between the instrument, such as MO, and the objective, stable prices, begins to weaken. As soon as a monetary authority attempts to regulate the money supply to reduce inflationary pressure, the stable relationship that might have existed between money (M) and prices (P) will break down, and attempting to control M is likely to fail. Therefore, rather than control the money supply, which is perhaps uncontrollable, monetary authorities control monetary conditions by setting short term interest rates, which work via their effect on the demand for money, rather than supply.

See also: Banking regulation