An image of a light bulb.

Productive Efficiency

What is Productive Efficiency?

Productive efficiency is a key concept in economics that refers to a situation when firms or economies produce maximum output at the lowest possible cost. It is also called production efficiency.

It means that minimum resources are used to produce maximum output. The following two cases can define productive efficiency:

- Maximum output is produced by using a given amount of available inputs.

- Given output is produced at the lowest possible cost by using minimum resources.

Basic Terms

Economic Efficiency

Economic efficiency is said to exist when scarce resources are used in the ‘best’ possible way, i.e., when the maximum of infinite wants are satisfied by using scarce resources. It means that minimum resources are used to produce maximum output, which will satisfy maximum wants. Productive efficiency is one type of economic efficiency. Other kinds of efficiency are allocative efficiency, pareto efficiency, and dynamic efficiency.

Efficient Resource Allocation

Resources are said to be efficiently allocated if they are being used in the ‘best’ possible way, i.e., the maximum of infinite wants are satisfied by using scarce resources. This will lead to maximum satisfaction in the economy. It is also called optimum resource allocation. Efficient resource allocation is always desirable because it represents the best possible solution to the economic problem of limited resources and unlimited wants.

Productivity vs. Efficiency

Productivity is the ratio between output and inputs, while efficiency means producing more output by using fewer inputs. Productivity is a measure of efficiency. An increase in productivity means an increase in efficiency.

Levels of Productive Efficiency

Productive efficiency can be discussed at three different levels: for a firm, a market, and a country.

Productive Efficiency for a Firm

For a firm, productive efficiency means producing output at the lowest point of the lowest average cost (AC) curve, i.e., the minimum average cost or unit cost. For a firm, productive efficiency has two parts.

Technical Efficiency

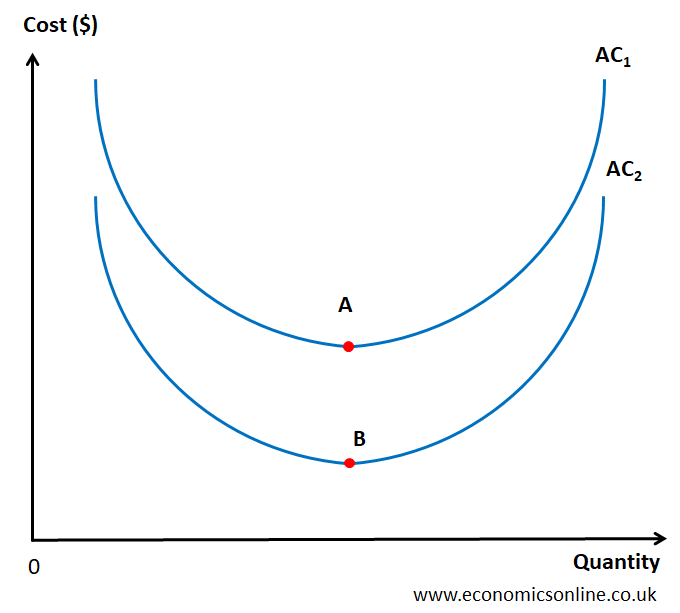

Technical efficiency means producing output at the lowest point of the average cost curve, where the marginal cost (MC) curve intersects the average cost (AC) curve. (MC=AC is the condition for the minimum point on any average cost curve.)

In the above diagram, points A and B are technically efficient because they are the lowest points on the average cost curves AC1 and AC2, respectively.

X-Efficiency

X-efficiency means producing output at the lowest average cost (AC) curve.

All points on AC2 are X-efficient because AC2 is the lowest average cost curve.

In the above diagram, point B is technically efficient as being the lowest point on AC2, and it is also X-efficient as being the point on the lowest average cost curve, AC2. Hence, point B shows productive efficiency.

Productive Efficiency for a Market

For a market, productive efficiency means producing output at the lowest average cost by all firms in that market. This happens only in perfect competition and is explained in the next section of this article.

Productive Efficiency for a Country

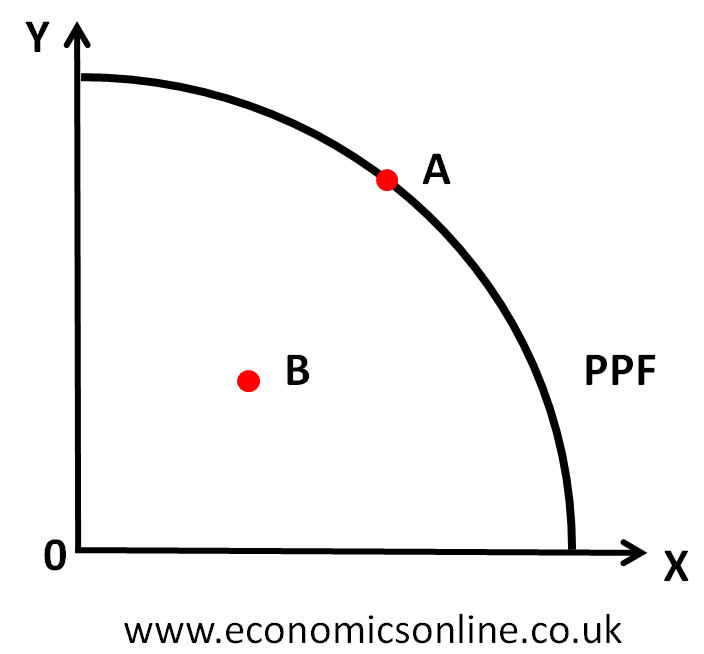

For a country, productive efficiency means producing output at any point on its production possibility frontier (PPF curve). It means the output is produced at maximum capacity and all the firms in a country are productively efficient.

In the above diagram, the horizontal axis (x-axis) has the quantity of good X, and the vertical axis (y-axis) has the quantity of good Y. Point A shows productive efficiency for a country. For all production levels on PPF, it is not possible to produce more quantity of good X without sacrificing some quantity of good Y because of limited resources. Point B shows productive inefficiency because it shows lower output, but it is possible to produce more goods with the available resources.

Productive Efficiency in Different Types of Markets

Productive Efficiency in Perfect Competition

Perfect competition is the only type of market structure where firms have productive efficiency.

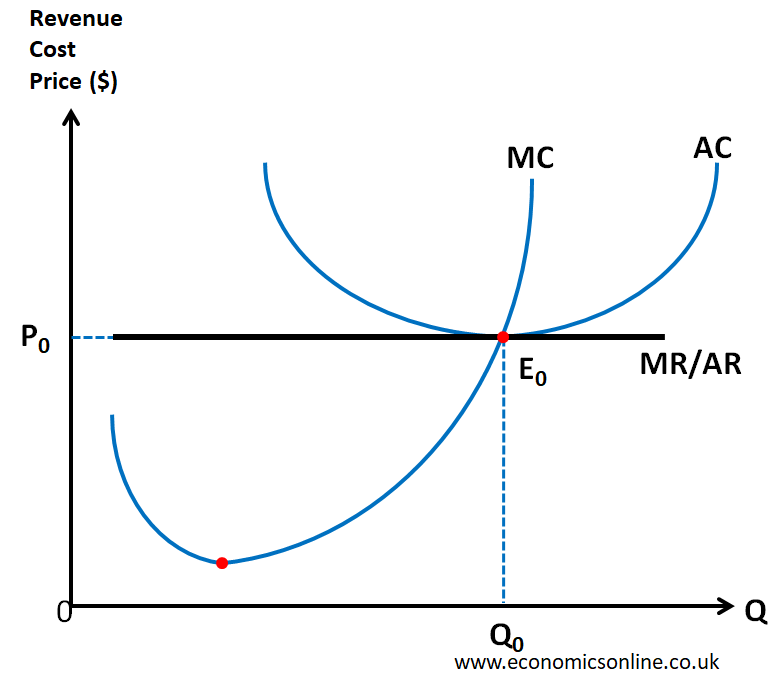

The above graph illustrates the long run equilibrium of a firm operating in perfect competition at point E0, where marginal revenue is equal to marginal cost (MR=MC) for output Q0.

We can see that, at output Q0, average cost (AC) is minimum (MC=AC) at point E0. Hence, the firm has productive efficiency in perfect competition.

Productive Efficiency in Monopolistic Competition

Firms in monopolistic competition are not productively efficient.

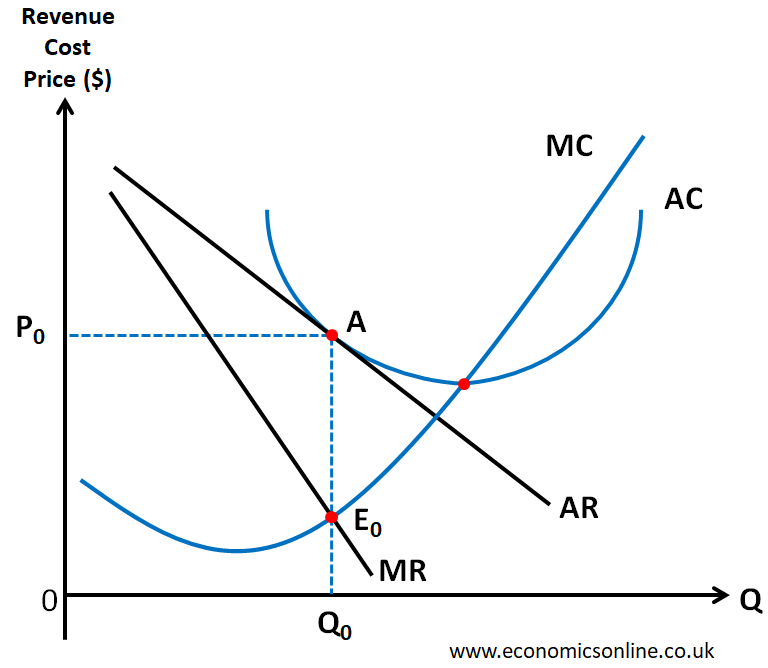

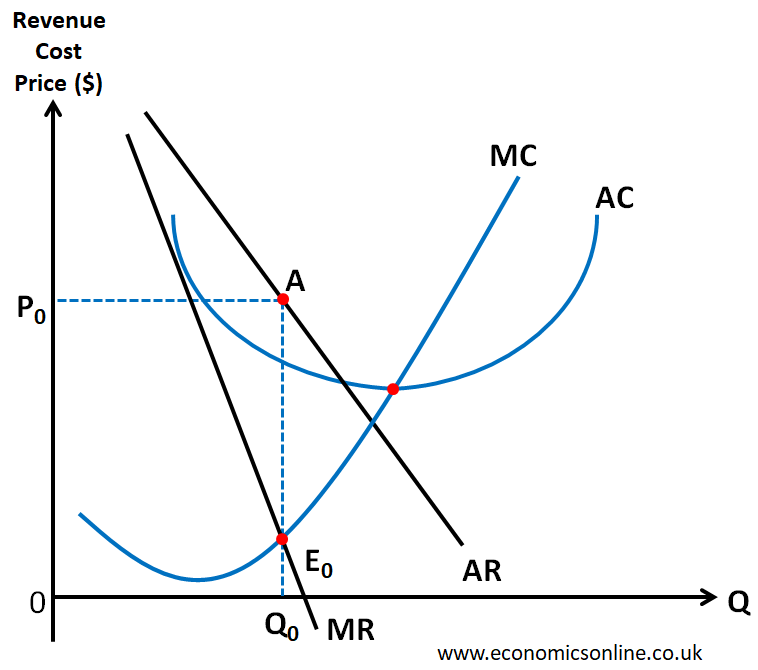

The above diagram illustrates the long run equilibrium of a firm operating in monopolistic competition at point E0, where marginal revenue is equal to marginal cost (MR=MC) for output Q0.

We can see that, at output Q0, AC = Q0A, which is not the minimum. So the firms operating in monopolistic competition are not productively efficient.

Productive Efficiency in Monopoly

In the case of monopolies, firms are not productively efficient.

The above diagram illustrates the long run equilibrium of a firm operating in monopoly at point E0, where marginal revenue is equal to marginal cost (MR=MC) for output Q0.

We can see that, at output Q0, AC = Q0A, which is not the minimum. So the firms operating in monopolies are not productively efficient.

The same is true for the collusive and non-collusive models of oligopoly in which firms do not have productive efficiency.

Hence, productive efficiency exists only in the case of perfect competition.

Importance of Productive Efficiency

Productive efficiency is a vital concept in economics because it ensures that scarce resources are used in the best possible way to produce the maximum possible output.

Is Productive Efficiency Achievable?

Achieving productive efficiency is desirable but not always easy in real-life situations. In the real world, markets are imperfect and firms are not productively efficient. For example, in monopolies and oligopolies, firms don’t reach the lowest point of the average cost curves in pursuit of profit maximisation, resulting in lower levels of output.

Similarly, a country may not produce output at a point on its production possibility curve (PPC), which leads to inefficient resource allocation.

Other Types of Economic Efficiency

Allocative Efficiency

Allocative efficiency means producing output as desired by the people of the country.

Pareto Efficiency (Pareto Optimality)

A situation is called Pareto-efficient if it is impossible to make someone better off without making someone else worse off. This efficiency occurs at PPF, where increasing the output of one good involves opportunity costs.

Productive Efficiency vs. Allocative Efficiency

It is important to distinguish productive efficiency from allocative efficiency. While productive efficiency focuses on minimising costs, allocative efficiency is about producing goods that are desired by people in order to satisfy their needs and wants. A firm may be productively efficient if it produces output at the lowest cost. But if that output is not according to the wants of people, the same firm will not be allocatively efficient.

Conclusion

In conclusion, the concept of productive efficiency means producing maximum output at minimum cost. The goal here is to utilise scarce resources in the best possible way. When firms and countries try to achieve productive efficiency, they actually improve the use of resources in the best way possible. Achieving productive efficiency should not be a one-time effort but a continuous journey towards excellence in resource allocation.