An image of man toy collecting money.

Pros and Cons of Capitalism

What is Capitalism?

Capitalism refers to an economic system characterised by private ownership of resources, profit motive, and price mechanisms with no or little government intervention in resource allocation. It is also called a free-market economy or free enterprise economic system.

Capitalism, like any other economic system, also answers the following three fundamental economic questions about resource allocation:

- What to produce?

- How to produce

- For whom to produce?

In capitalism, these questions are answered by households and firms through freedom of choice and the price mechanism, with minimum government intervention.

Capitalism is supported by economists Adam Smith and Milton Friedman in their writings.

Key Characteristics of Capitalism

Private Ownership of Resources

The private ownership of means of production and private property are major features of capitalism. It means that individuals have the right to own, control, and dispose of land, buildings, machinery, and other natural and man-made resources.

The government provides property rights through the legal system. Private ownership of factors of production not only refers to the right to own and dispose of real assets; it also gives the owners of resources the right to earn income (rewards) from the resources they own.

Self Interest

Since capitalism is based on the principle that individuals should be free to do as they wish, the motive for economic activity is self-interest. Each economic agent in capitalism will make decisions purely based on self-interest. Firms will try to maximise profit. Consumers will spend money to maximise their satisfaction.

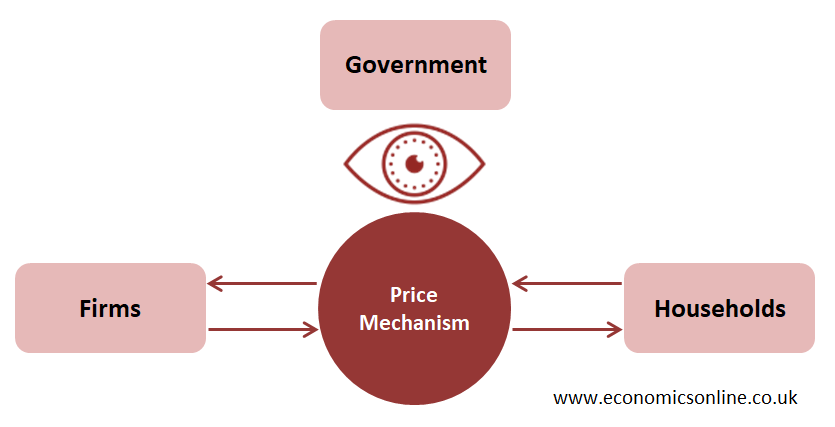

Price Mechanism

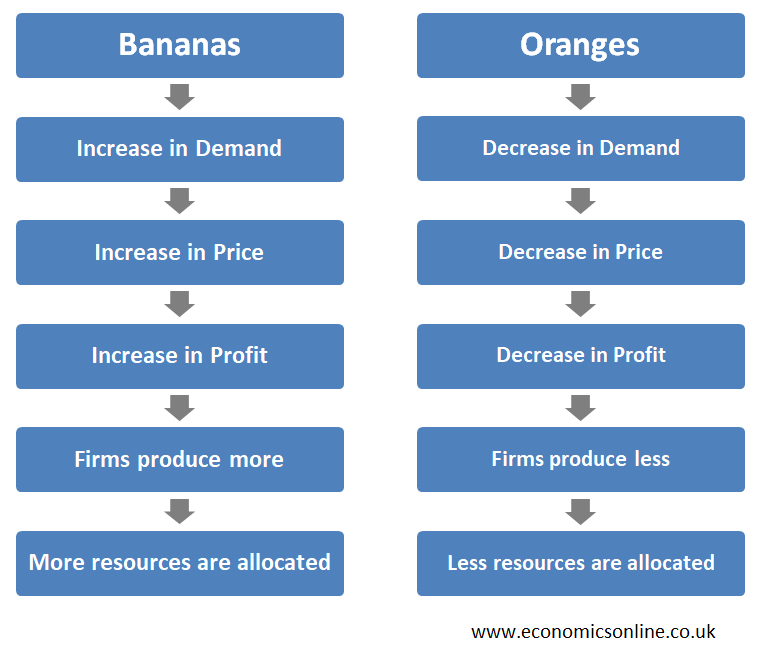

It means that resource allocation decisions are taken by producers and consumers with no government intervention. In a free market, the interaction of demand (consumers) and supply (producers) determines the price and quantity. A change in price is used as a mean to allocate resources.

The decisions of producers determine the supply of a product; the decisions of buyers determine the demand. The interactions of demand and supply bring about a change in the price, which leads to resource allocation decisions.

The above figure shows the effect of demand for bananas increasing while demand for apples decreases.

- If consumers are willing to pay a higher price for a product, producers will allocate more resources to produce that product.

- If consumers are willing to pay a low price for a product, producers will allocate fewer resources to produce that product.

- Resource Allocation is changing all the time in response to changes in consumer demand and the costs of production.

- Resources move towards those products for which demand is rising.

- Resources move away from those products for which demand is falling.

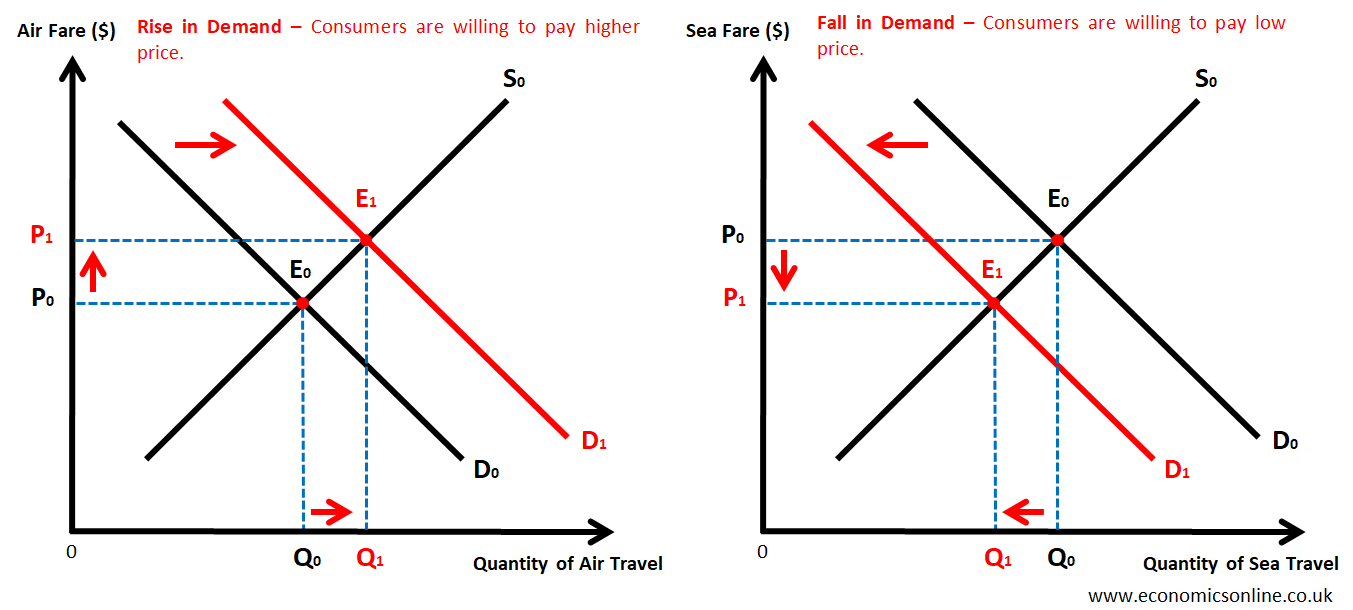

Let’s illustrate this with diagrams.

The above graph shows how resources are moved from sea travel to air travel through price mechanism.

Freedom of Enterprise and Choice

Freedom of enterprise means that individuals are free to buy and hire economic resources, to organise these resources for production, and to sell their products in markets of their own choice.

The consumer is regarded as being sovereign since the way in which he or she chooses to spend his income determines the ways in which society uses its economic resources. In capitalism, producers respond to consumers' preferences; they produce what consumers demand.

Competition

Economic rivalry, or competition, is another essential feature of capitalism. It means there are many sellers of a product who compete for the consumers spending. Competition, whether actual or potential, should also result in low prices and better quality. Actual Competition means the number of existing rival firms in the industry. Potential Competition means the number of firms that might enter the market in the future in case of higher profits. This means it is easy for firms to enter or leave the industry. Efficient firms (with low cost) will stay in the market. Inefficient firms (with high cost) will go out of the market. Firms, who respond to changes in consumer demand, will earn high profits. Profit will be an incentive to innovate and expand.

Role of Government

The government has no direct role in the workings of capitalist societies and it does not interfere in the operation of the price mechanism. It ensures law and order through the police and judiciary. It also ensures property rights. It prints and circulates money. In pure capitalism, the government's role is to watch what is happening and make no intervention. In real life, governments intervene when the price mechanism does not provide the best allocation of resources (market failure). Governments provide Public Goods like defence and street lights. Governments also provide merit goods like healthcare and education.

Pros and Cons of Capitalism

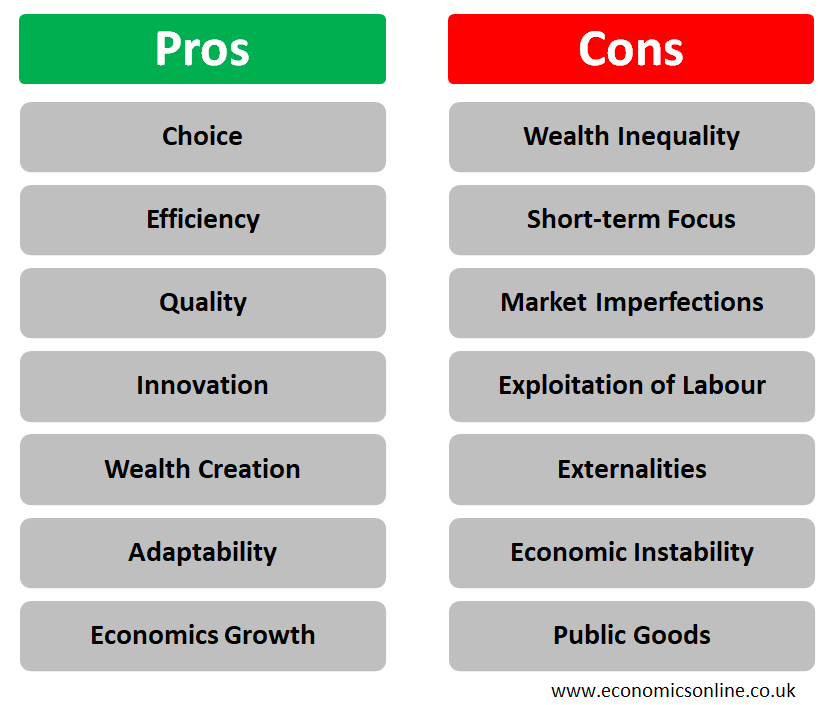

Pros of Capitalism

Choice

One benefit of capitalism is choice. If there are a large number of firms producing a product, consumers will have a choice of producers. This means many firms are trying to meet the demand from customers. This means that consumers have economic freedom and sovereignty. Hence, consumers determine what is produced in capitalism.

Efficiency

In capitalism, costs and prices may be low. The profit motive and competition promote efficiency. Firms have the freedom to produce the most desirable goods (allocative efficiency) with least cost methods (productive efficiency). Competition also leads firms to charge lower prices due to lower costs and to attract more customers.

Quality

In capitalism, quality of the goods and services may be high. Market forces can promote the improvement of methods of production and a rise in the quality of products made. It does this by putting competitive pressure on firms, and by providing them with the profit incentive to try to gain more sales by making their products more attractive to consumers.

Innovation

Capitalism provides an incentive for innovation and entrepreneurship. In a capitalist economy, individuals have the opportunity to pursue their own business ideas and take calculated risks. The chance of earning profits motivates entrepreneurs to develop new products, technologies, and services that meet consumers' needs and preferences. This drive for innovation fosters economic development and improves living standards.

Wealth Creation

In a capitalist system, people can create their own wealth, leading to prosperity. By allowing individuals and businesses to pursue profit opportunities, capitalism creates the conditions for economic growth. As businesses expand and succeed, they generate jobs, increase wages, and contribute to overall prosperity. The accumulation of wealth in the hands of individuals and businesses can be reinvested into the economy, leading to further economic expansion and the potential for greater prosperity for society as a whole.

Adaptability

Capitalism has the ability to adjust to changing market conditions, technological advancements, and consumer demands. Capitalist economies can respond quickly to disruptions, such as economic recessions, by reallocating resources and adjusting prices. The competitive nature of capitalism encourages businesses to be agile and innovative, enabling them to survive and thrive in dynamic environments. This adaptability ensures that capitalism remains a robust and flexible economic system.

Economic Growth

The pursuit of profit and the freedom to engage in market transactions incentivise individuals and businesses to invest, expand production, and create wealth. As a result, capitalist economies often experience higher rates of economic growth compared to other economic systems. Economic growth leads to increased employment opportunities, higher incomes, and improved living standards for individuals and communities.

Moreover, through choice, competition and innovation, capitalism drives technological advancements, increases productivity, and lowers production costs. This leads to the availability of a wider range of goods and services at more affordable prices, allowing individuals to enjoy a higher standard of living.

Cons of Capitalism

Wealth Inequality

Under capitalism, there is a significant risk of wealth inequality through its concentration in the hands of a few individuals, firms or groups. There may be unequal distribution of wealth, with some people being very rich, and others being very poor. This leads to a substantial gap between the rich and the poor.

Differences in income will increase over time. Those earning high incomes can afford to save and buy shares. Their savings and shares will earn them interest and dividends (a share of profits). In contrast, the poor cannot afford to save. Critics argue that capitalism fails to provide equal opportunities for all individuals to succeed.

Short-term Focus

Critics argue that capitalism often encourages a short-term focus on financial gains rather than long-term sustainability. The profit motive may lead businesses to prioritise immediate profits over broader societal concerns, such as environmental sustainability for future generations or social well-being.

Moreover, rich people can have more influence over what is produced due to their higher purchasing power. As a result, more resources will be allocated for luxuries and fewer resources will be allocated for necessities.

Market Imperfections

One of the disadvantages of capitalism is the possibility of market imperfections. A market may become dominated by one firm (a monopoly) or a few firms (an oligopoly). For instance, due to its monopoly power, a firm can exploit consumers by charging higher prices. These powerful firms can increase prices and limit the choice of customers. Moreover, in monopolies and oligopolies, resources are not efficiently allocated.

Exploitation of Labour

Capitalism's profit-driven nature can encourage the exploitation of labour in the form of lower wages. In the pursuit of maximising profits, some businesses may prioritise cost-cutting measures, such as low wages, poor working conditions, and limited benefits. This can lead to the exploitation and mistreatment of workers in labor markets, particularly in industries where labour rights are not adequately protected. Capitalism fails to provide not only equality of outcome but also equality of opportunity.

Externalities

Capitalism may neglect the negative externalities associated with certain economic activities. Consumers and private firms may only consider private costs and benefits when making consumption or production decisions. External costs and external benefits will be ignored. For instance, pollution caused by industrial production may harm the environment and public health, but the costs associated with these damages are often not factored into the market price. This failure to internalise external costs can result in environmental degradation, resource depletion, and negative societal impacts that are not adequately addressed within the capitalist framework.

Economic Instability

One of the inherent risks of capitalism is economic instability. The pursuit of profit and the fluctuations of supply and demand can lead to boom and bust cycles, causing recessions and economic crises.

Public Goods

In the absence of government interventions, public goods and public services will not be produced by firms in capitalism. Private firms cannot charge a price for public goods because of their non-excludability and non-rivalry features. Moreover, in capitalism, merit goods (goods with positive externalities) are underproduced, and de-merit goods (goods with negative externalities) are overproduced. This means that the resources are not properly allocated for merit, de-merit, and public goods.

Conclusion

In conclusion, capitalist countries have an economic system characterised by private ownership, profit motive and price mechanism with almost no government intervention. There are many advantages of capitalism, yet, in the absence of government intervention, there may be many disadvantages as well, including wealth inequality, market imperfections, under-provision of merit goods, externalities, and many more. In real life, governments intervene in markets when they fail to allocate resources efficiently.